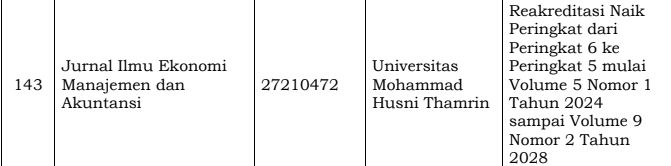

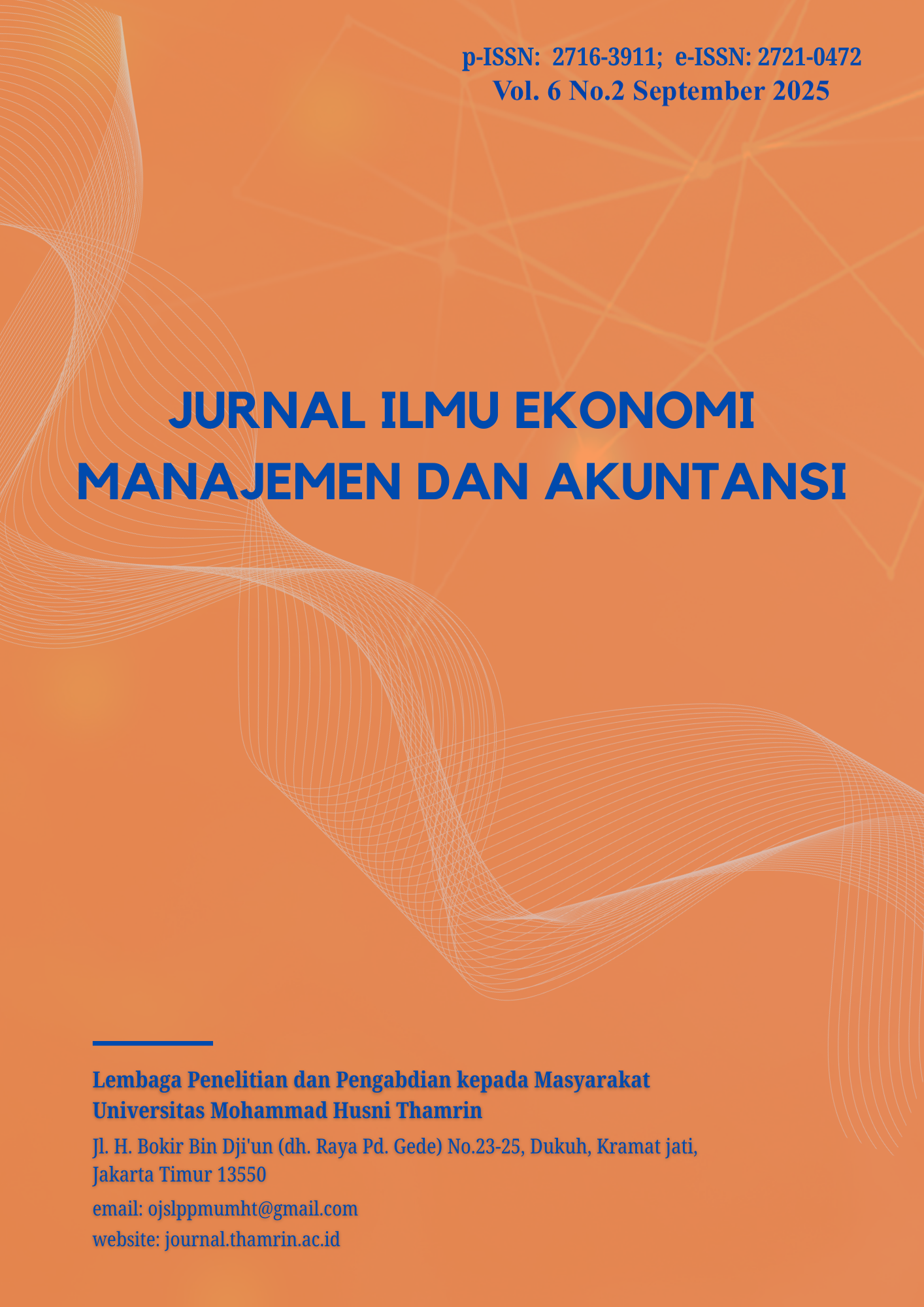

The Use of Digital Forensic Accounting Techniques in Occupational Fraud Detection and Prevention: A Literatur Review

DOI:

https://doi.org/10.37012/ileka.v6i2.3062Abstract

Digital forensic accounting is a rapidly growing field in modern accounting, combining traditional investigative methods with cutting-edge digital technology to uncover and prevent financial fraud. One type of fraud that is a major concern in the corporate and organizational world is occupational fraud. Occupational fraud is fraudulent acts committed by employees, managers, or related insiders intended to gain personal gain at the expense of the organization. This study aims to examine the role and effectiveness of using digital forensic accounting techniques in detecting and preventing occupational fraud through a literature review of ten research articles published between 2023 and 2025. The results of the study show that developments in digital technology such as Artificial Intelligence (AI), Machine Learning (ML), Big Data Analytics, Blockchain, Digital Forensic Tools, Intelligent Automation and Deep Learning Tools have had a significant impact on improving the accuracy, speed, and efficiency of the fraud detection and investigation process. The application of these technologies enables forensic auditors to identify suspicious transaction patterns in real time, strengthen internal control systems, and improve the transparency of organizational financial data. However, the study also found challenges in the form of limited human resources with technological expertise, lack of data integration between organizational units, and data security and ethics issues. Overall, digital forensic accounting has proven to be a strategic instrument in supporting the prevention and detection of occupational fraud in the era of digital transformation.

Downloads

Published

Issue

Section

Citation Check

License

Copyright (c) 2025 Norine Arifah Aini, Nova Fitriana, Rizka Rahma Yuliani, Hastanti Agustin Rahayu

This work is licensed under a Creative Commons Attribution 4.0 International License.

Jurnal Ilmu Ekonomi Manajemen dan Akuntansi (ILEKA) Universitas Mohammad Husni Thamrin allows readers to read, download, copy, distribute, print, search, or link to the full texts of its articles and allow readers to use them for any other lawful purpose. The journal allows the author(s) to hold the copyright without restrictions. Finally, the journal allows the author(s) to retain publishing rights without restrictions Authors are allowed to archive their submitted article in an open access repository Authors are allowed to archive the final published article in an open access repository with an acknowledgment of its initial publication in this journal.

Jurnal Ilmu Ekonomi Manajemen Akuntansi (ILEKA) Mohammad Husni Thamrin is licensed under a Creative Commons Attribution 4.0 International License.