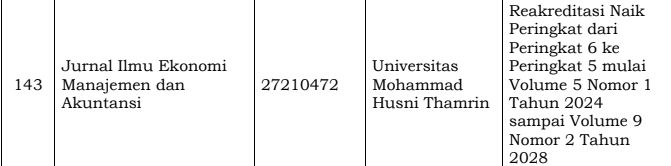

Convergence of IFRS with Local Accounting Standards: A Literature Review

DOI:

https://doi.org/10.37012/ileka.v6i2.3042Abstract

Accounting is often described as the “global language of business,” as it presents financial data that is easily understood, compared, and used continuously by various parties across countries. The convergence of Indonesian Reporting Standards (IFRS) with Indonesian Financial Accounting Standards (SAK) in Indonesia is a strategic step in improving the quality of financial reporting and strengthening national economic competitiveness. However, convergence is not without challenges. IFRS implementation demands professional preparedness from accountants, auditors, and regulators because principles-based standards require careful interpretation. Furthermore, differences in Indonesia's legal and economic context necessitate certain adjustments in PSAK. This study uses a library research approach by reviewing five scientific articles published between 2020 and 2025 that are relevant to the topic of IFRS-SAK convergence. The results of the literature review indicate that IFRS convergence contributes to increased transparency, comparability, and value relevance of financial reports, primarily through the application of fair value accounting. Furthermore, convergence has been shown to suppress earnings management practices in certain sectors, particularly banking, and improve the credibility of financial reports in the eyes of global investors. However, the effectiveness of convergence is not solely determined by standards, but is also influenced by institutional factors such as corporate governance, audit quality, and regulatory consistency. This study contributes academically to enriching the discourse on the harmonization of accounting standards, and practically provides recommendations for regulators, auditors, and reporting entities in strengthening the implementation of IFRS in Indonesia.

Downloads

Published

Issue

Section

Citation Check

License

Copyright (c) 2025 Yuliana Dewi Siregar, Rodiah Aprilia, Dilla Ayu Kartika, Jufri Darma

This work is licensed under a Creative Commons Attribution 4.0 International License.

Jurnal Ilmu Ekonomi Manajemen dan Akuntansi (ILEKA) Universitas Mohammad Husni Thamrin allows readers to read, download, copy, distribute, print, search, or link to the full texts of its articles and allow readers to use them for any other lawful purpose. The journal allows the author(s) to hold the copyright without restrictions. Finally, the journal allows the author(s) to retain publishing rights without restrictions Authors are allowed to archive their submitted article in an open access repository Authors are allowed to archive the final published article in an open access repository with an acknowledgment of its initial publication in this journal.

Jurnal Ilmu Ekonomi Manajemen Akuntansi (ILEKA) Mohammad Husni Thamrin is licensed under a Creative Commons Attribution 4.0 International License.